A lien can turn a normal property matter into a stressful one fast. You may be getting ready to sell a rental, refinance, renew insurance paperwork, or deal with a tenant dispute, and then a title search shows a claim you didn’t expect. That claim can stall everything.

For Texas landlords and property owners, the good news is that most lien problems can be worked through with a clear plan. The right answer depends on the type of lien, who filed it, whether the debt is valid, and how quickly you need the title cleared. A paid mortgage lien is handled differently than a mechanic’s lien from a contractor, and both are different from a judgment lien or a tax lien.

If you’re trying to figure out how to release lien on property, start with one principle. Don’t guess. Pull the actual filing, confirm what was recorded, and match your next move to the specific lien in front of you.

That Sinking Feeling When You Discover a Lien on Your Property

A common Texas landlord scenario goes like this. You’re under contract to sell a rental house, or you’re trying to refinance, and the title company says there’s a lien in the county records. Sometimes it’s a contractor you never hired directly. Sometimes it’s an old deed of trust that should have been released years ago. Sometimes it traces back to a judgment or tax issue.

That moment causes the same reaction almost every time. You want to know whether the lien is real, whether it blocks the sale, and how long it will take to fix.

A lien is a claim against property. In practical terms, it clouds title. That means buyers, lenders, and title companies usually won’t move forward until the claim is resolved, bonded around, released, or otherwise cleared. For landlords, that can also create side problems with lease enforcement, turnover planning, repairs, and property management decisions.

Some liens are voluntary. Your mortgage is the obvious example. Others are involuntary, like mechanic’s liens, judgment liens, and tax liens. If you’re sorting out whether unsecured debt can become a property problem, this overview on understanding credit card debt and your home gives useful background on when a debt claim can end up affecting real estate.

Texas law gives property owners real tools, but the steps matter. The first useful move is usually not a phone call. It’s record verification. If you need a quick legal primer on the basic concept, this page on release of liens definition is a good starting point.

A lien problem feels urgent because it is urgent. But urgency doesn’t mean rushing blind. The fastest clean resolution usually starts with the county records.

First Steps How to Identify and Verify a Lien

Before you pay anyone, argue with anyone, or promise a closing date, confirm exactly what was filed.

Start with the county real property records

In Texas, liens affecting real estate are usually found in the county records where the property sits. Many county clerks have online search tools. In larger counties, owners often begin there and then confirm details with the clerk’s office or a title company if something looks unclear.

Search using more than one identifier:

- Owner name: Search the current owner and any prior owner connected to the issue.

- Property address: Helpful, but not always enough by itself.

- Legal description: This is often the most reliable match.

- Recording data: If a title company gave you a clerk’s file number or instrument number, use it.

You’re looking for the actual recorded document, not just a summary line on a search screen.

Pull the key facts from the recorded document

Once you find the filing, extract the details that control your next move.

A useful working list includes:

Who filed it

The claimant may be a lender, contractor, creditor, tax authority, or someone acting through counsel.What kind of lien it is

Look for labels such as Release of Lien, Deed of Trust, Mechanic’s Lien, Affidavit Claiming Lien, Abstract of Judgment, or tax-related filings.When it was recorded

Filing date matters for priority, deadlines, and whether a limitations argument may exist.What property it describes

Check the legal description carefully. Liens sometimes get tied to the wrong tract or use an incomplete description.Whether the debt appears paid, disputed, or unresolved

A lien can remain in the records even after the underlying debt was satisfied.

When a title report is worth the cost

For many owners, a preliminary title report is the cleanest way to confirm what’s attached to the property. According to ProTitle USA’s explanation of lien removal steps, the primary method to release a voluntary lien begins with obtaining a preliminary title report from a title company to verify lien details, including the recording number and lienholder, and that can cost $100-$500. The same source states that after payment, the lienholder issues a Release of Lien that must be filed with the county clerk, and that success rates exceed 95% for paid liens but drop to 40% without legal counsel due to filing errors.

That last point matters. In practice, many lien problems don’t stay unresolved because the debt is impossible to fix. They stay unresolved because the release document is wrong, unsigned, missing notarization, or never gets recorded.

Practical rule: Don’t rely on an email saying the debt is paid. Until a proper release is recorded and confirmed, title may still be clouded.

What landlords should watch for

Landlords face a few recurring lien patterns that owner-occupants often don’t:

| Issue | Why it matters |

|---|---|

| Tenant-arranged repairs | A contractor may claim authority came from the occupant, even if the lease didn’t allow the work |

| Turnover renovations | Multiple vendors increase the chance of unpaid subcontractor claims |

| Prior management problems | A former manager may have left unresolved bills or incomplete project records |

| Old financing | A prior loan may have been paid off but never properly released |

If the lien touches repairs, contractor payment, or project notices, review the underlying job records right away. Pull the lease, work orders, invoices, text messages, and payment proof. Those documents often decide whether you’re dealing with a valid claim, a filing defect, or a negotiation problem.

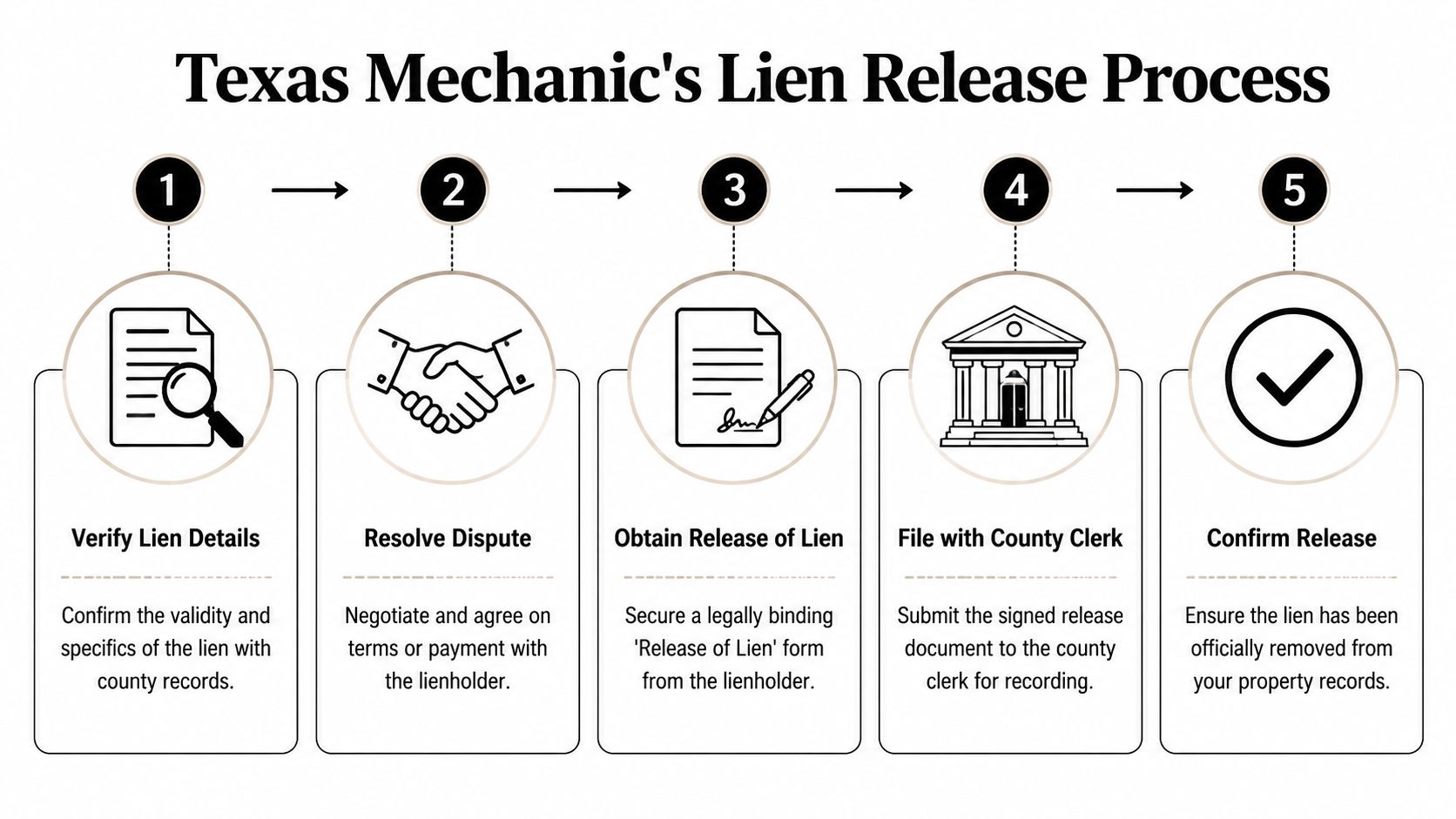

Releasing a Mechanic's Lien in Texas

Mechanic’s liens create some of the hardest title problems for landlords because they often arise during repairs, turnover work, or emergency maintenance. The trouble gets worse when a tenant called a contractor directly, a property manager approved work without clear authority, or a general contractor failed to pay a subcontractor.

What Texas law allows

Texas Property Code Section 53.157 provides six statutory methods to discharge mechanic’s liens. More than 25,000 such claims are filed annually in Texas, and one common discharge method is filing a notarized Release of Lien after payment. Another common method, used in 40% of discharges in urban counties, involves posting a surety bond for 1.5 times the lien amount to clear title while the dispute continues, as described in this discussion of lien release and removal in Texas.

If you want the broader statutory framework, review Texas Property Code Chapter 53. That chapter controls many of the notice, perfection, filing, foreclosure, and release issues tied to construction liens.

A landlord example that comes up often

A tenant reports a habitability issue. Wanting the problem fixed quickly, the tenant hires someone without written authority under the lease. The contractor does the work, doesn’t get paid, and then files a lien claim against the property.

The first question isn’t whether the work happened. It’s whether the lien was validly created under Texas law and whether the person authorizing the work had legal authority to bind the owner. Those are not the same thing.

What works in real life

For a mechanic’s lien, owners usually make progress through one of these paths:

- Pay and obtain a proper release: This works when the debt is valid, the amount is acceptable, and speed matters more than fighting.

- Negotiate a reduced resolution: This can work when there’s a billing dispute, incomplete work, or a shared responsibility problem.

- Challenge the lien’s validity: This makes sense when required notices, deadlines, signatures, or statutory elements are missing.

- Bond around the lien: This is often the best business solution when a sale or refinance can’t wait.

What usually does not work is sending a casual email saying the lien is invalid and assuming the problem will disappear.

The basic release path after payment

If the claim is legitimate and you decide to resolve it, the cleanest route is usually:

- Confirm the recorded lien document.

- Match the lien amount against the contract, invoices, and proof of work.

- Pay under a written settlement that requires a signed notarized release.

- File the executed release in the county real property records.

- Confirm the clerk indexed it correctly and the title company accepts it.

A release that is signed but not recorded may still leave your title problem unresolved.

Sample demand language after satisfaction

If you’ve paid and the claimant is dragging their feet, your written demand should be plain and direct. For example:

Please provide a signed and notarized Release of Lien for the claim recorded against the property at [property description], under clerk’s file number [number]. The underlying obligation has been satisfied. Please return the executed release in recordable form immediately so it can be filed in the county real property records.

That kind of letter should attach proof of payment and identify the exact recorded lien.

Tenant-related repair disputes need extra care

Texas landlords should be especially careful when the lien traces back to repairs requested by a tenant. The lease may limit what the tenant can authorize. Texas Property Code Section 92 often shapes repair duties, notice issues, and habitability disputes, but it does not automatically mean a tenant had authority to hire a contractor who can bind the owner’s title.

Don’t confuse a repair complaint with authority to create an owner obligation. Those are separate legal questions.

Where the facts are mixed, the practical decision often comes down to timing. If a closing is near, bonding around the lien or negotiating a release may be smarter than litigating first. If no transaction is pending, a direct challenge to the lien’s validity may be the better long-term move.

How to Remove Judgment Liens from Your Property

A judgment lien is different. It doesn’t usually start with construction work or repairs. It starts with a lawsuit, a money judgment, and then a creditor recording an abstract of judgment in the county records.

For property owners, the practical issue is simple. Once recorded, that judgment filing can attach to non-exempt real property in the county and interfere with a sale or refinance. Landlords often discover these liens during title review, not when the judgment is entered.

Start with the judgment itself

Pull the court case and the recorded abstract. You need to know:

- The exact creditor name

- The amount claimed

- Whether interest or costs were added

- The county where it was recorded

- Whether the property is homestead or non-homestead

If the property is your principal residence, Texas homestead protections can be critical. A judgment lien that appears in the records may still require action to clear title, but homestead status can change whether the lien validly attaches in the first place.

The usual path to release

Most judgment lien problems are solved by satisfaction or settlement. Once that happens, the creditor should provide a release in recordable form.

Texas law reflects a broader expectation that lienholders act promptly after payment. Under Texas Property Code Section 12.017 and this discussion of lien releases, lenders must file a release of lien within 60 days after a home loan is paid off, and that deadline shortens to 30 days if the borrower makes a written request. That statute addresses home loans, but it reflects an important practical principle for all lien matters. Once the obligation is satisfied, the title records should be updated without delay.

For judgment liens, don’t assume the creditor will handle that automatically. Ask for the signed release, confirm it is recordable, and verify that it was filed.

Homestead issues often change the strategy

If the property is your Texas homestead, the right move may be a demand for a partial release tied to homestead protection. That can be especially important where the creditor recorded broadly and the title company wants a cleaner record before closing.

For background on aggressive judgment collection tools, The MCA Guide's insights on judgments help explain why owners should pay close attention to what was signed, what was entered, and what was later recorded.

If you need to understand the filing itself, this overview of a Texas abstract of judgement is useful.

A good checkpoint before you celebrate

Many owners stop too early. They settle the judgment, save the receipt, and assume the title issue is gone. It isn’t gone until the release is in the county records and the title company confirms clearance.

A short walkthrough can help if you want to see the process from a consumer-facing perspective:

Keep this in mind: Payment resolves the debt. Recording the release resolves the title problem.

Resolving Property Tax Liens and IRS Liens

Government liens operate by different rules. Owners often assume every lien can be handled with the same release form, but tax matters rarely work that way.

Texas property tax liens

For delinquent Texas property taxes, the issue usually isn’t getting a private creditor to sign a standard release. The tax claim is tied to the unpaid taxes and is typically resolved through payment or an approved arrangement with the taxing authority.

That means your first call is often to the county tax assessor-collector or the lawyer handling collection. Ask for the current payoff and how the account will be updated after payment. Then confirm what the title company will need to see.

In practice, owners should gather:

- Current tax statements

- Delinquency notices

- Any payment plan documents

- Proof of recent payments

- Contact information for the collection office

A title company may require direct confirmation that the balance has been resolved before it will insure around the issue.

IRS liens

Federal tax liens are more formal and usually require more paperwork. If the full debt is paid, the IRS process for release is different from the county-level tax process. In some situations, owners also look at discharge or subordination options when they need to sell or refinance a specific property before the full tax issue is completely resolved.

For a practical overview of those options, federal tax lien solutions can help you understand the difference between release, discharge, and subordination.

Why timing matters more than owners expect

Tax problems tend to get worse when owners wait for a transaction deadline. A buyer is already lined up. The lender has issued a commitment. Then someone realizes taxes are delinquent or a federal filing is still active.

That pressure is one reason property disputes have felt more volatile in recent years. According to this discussion of property lien options and recent Texas legislation, there was a 35% rise in lien filings after the post-2024 floods, and 40% of those were invalidated under new rules. That source discusses mechanic’s liens on residential rentals, but the broader lesson is useful for tax matters too. Property issues can escalate quickly after disruptive events, and delayed attention usually narrows your options.

What owners should do first

For government liens, a clean sequence usually works best:

| Lien type | First move | Main goal |

|---|---|---|

| Property tax lien | Contact the county tax office or collection counsel | Get an exact payoff or approved resolution path |

| IRS lien | Confirm the tax period and account status | Determine whether you need release, discharge, or subordination |

Government liens are less forgiving of incomplete paperwork. Keep every notice, every payoff letter, and every payment confirmation in one file.

Proactive Strategies Using Bonds and Lien Waivers

Sometimes the best answer isn’t removing the lien immediately by winning the argument. It’s removing the lien from the property while the argument continues somewhere else.

That’s where bonds and lien waivers become powerful tools for landlords, investors, and property managers.

When a bond solves the business problem

If a mechanic’s lien is disputed but you need clear title now, bonding around the lien can be the practical answer. The basic idea is simple. You post a surety bond in the required amount, file it properly, and shift the claimant’s security from the property to the bond.

That approach often makes sense when:

- A sale is pending: You can’t afford to let a disputed lien sit on title.

- A refinance is time-sensitive: The lender wants the property cleared before closing.

- The claim looks inflated: You want to challenge the amount without freezing the asset.

- The contractor dispute is real but unresolved: You need room to litigate or negotiate without losing the transaction.

This is often a business-first move, not an admission that the claimant is right.

Lien waivers prevent many disputes before they start

For landlords doing repairs or renovation work, lien waivers are one of the best prevention tools available. Use them during the project, not after a dispute begins.

A practical system looks like this:

- Get a written contract before work starts.

- Match every payment to a waiver.

- Require updated waivers from contractors and, where appropriate, downstream parties.

- Keep proof of payment with the waiver set.

- Review authority in the lease so tenants can’t create confusion about who may approve work.

Conditional waivers are generally tied to payment being received. Unconditional waivers are stronger but should be used carefully and only when payment has cleared.

What works and what doesn't

What works is documentation. Clear vendor agreements. Clear approval authority. Clear payment records. Clear waivers.

What doesn’t work is informal property management. If a tenant texts a handyman, the manager pays part of an invoice, and nobody collects a waiver, that is exactly the sort of record gap that later becomes a title problem.

For landlords, the lesson is simple. Lien removal matters. Lien prevention matters more.

If you need help with a lien, eviction, lease issue, or rental dispute, contact The Law Office of Bryan Fagan, PLLC for a free consultation today. A Texas landlord tenant lawyer can help you review the filing, protect your tenant rights or ownership rights under the Texas Property Code, and move quickly toward a practical solution whether you need title cleared, a repair dispute resolved, or support from an eviction attorney.