A lot of Texans reach owner financing after a frustrating few months.

The buyer has income, a down payment, and a real plan to pay, but the bank still says no. The seller has a house that isn’t moving, or wants monthly income instead of one lump sum at closing. Both sides start asking the same question: can we make this deal work ourselves?

Sometimes the answer is yes. An owner finance Texas home deal can open the door to a sale that would otherwise stall. But it only works well when the paperwork matches Texas law and both sides understand what happens if the relationship breaks down later.

That last part gets missed all the time. People think owner financing is just a handshake, a promissory note, and house keys. It isn’t. In Texas, these deals can drift into foreclosure issues, title problems, and even landlord-tenant disputes if the contract is drafted poorly. For buyers, that can put your possession at risk. For sellers, it can turn a simple sale into a costly fight over default, notices, and removal from the property.

If you're sorting through options, it also helps to understand that a huge cash down payment isn't always the only path to ownership. This guide on the need for a 20% down payment on a home gives helpful general context for buyers comparing traditional lending with more flexible arrangements.

The practical question isn’t whether owner financing is good or bad. The practical question is whether the structure protects your rights under the Texas Property Code, your contract, and the facts of your deal.

Considering an Alternative Path to Texas Homeownership

A common situation looks like this. A family finds a home they can afford month to month, but strict underwriting blocks the mortgage. At the same time, the seller owns the property free and clear, wants to move the home quickly, and is open to carrying the note.

That setup is why owner financing keeps coming up across Texas.

For some sellers, it’s a way to widen the buyer pool. For some buyers, it’s a path around rigid lending standards. But neither side should treat it like an informal side deal. A house sale with seller financing is still a serious credit transaction secured by real property.

Why people turn to owner financing

Banks often reject borrowers for reasons that don’t always reflect whether they can make the payment. Self-employed income, credit history issues, rural properties, and title quirks can all complicate conventional financing.

Sellers have their own reasons. Some want regular payments over time. Some want a faster, more flexible sale. Others are selling in areas where traditional mortgage lending is harder to place.

Practical rule: If the deal only works because everyone is “keeping it simple,” it usually isn’t simple enough to survive a default.

What makes these deals succeed

The good owner-financed home sale has structure. The bad one has assumptions.

A workable deal usually starts with clear expectations on:

- Payment terms that match the buyer’s actual budget

- Recorded documents that show who owns what and who can enforce what

- Default language that says exactly what happens if payments stop

- Property obligations for taxes, insurance, and repairs

- Exit planning so neither side is trapped later

That’s where legal drafting matters. In Texas, owner financing can overlap with foreclosure law, eviction procedure, title issues, and consumer protection rules. A buyer may think they’re purchasing a home. A seller may think they can just “take it back” if things go wrong. Both assumptions can lead to trouble.

What Is Owner Financing in a Texas Home Sale

In a Texas home sale with owner financing, the seller acts as the lender. Instead of a bank funding the purchase, the buyer makes payments directly to the seller under documents signed at closing.

The basic moving parts are familiar. There’s a purchase price, a down payment, an interest rate, and a repayment schedule. What changes is who is extending credit.

According to this Texas owner financing overview, owner financing interest rates in Texas typically average around 8%, with a common range of 4% to 10%. Sellers often require a 10% to 15% down payment, and these transactions can close 3 to 4 weeks faster than traditional sales.

How the transaction usually works

A practical owner-financed home deal often follows this pattern:

- The buyer and seller agree on the sale price and financing terms.

- The buyer pays an agreed down payment.

- The buyer signs a promissory note promising repayment.

- The parties sign security documents that let the seller enforce the debt if the buyer defaults.

- The closing documents are recorded, depending on the structure used.

The strongest version of this arrangement usually gives the buyer title at closing and gives the seller a recorded lien. That tends to be cleaner than informal possession-first arrangements.

A simple example

Assume a seller owns a home in East Texas and wants to sell to a buyer who has steady income but can’t qualify for a bank loan. The parties agree on price, down payment, monthly installments, taxes, insurance responsibilities, and late-payment rules. At closing, the buyer signs a note and related security documents, then begins paying the seller each month.

That sounds simple, but the document choice changes everything.

For readers who want a general background comparison with rural transactions, this explanation of what is owner-financed land is useful because it shows how seller-carried deals are often introduced. Homes, however, need more protection than raw land because occupancy, repairs, title transfer, and default remedies are more complicated.

Texas structures are not all equal

The phrase “owner financing” covers more than one legal setup. Some are much safer than others.

A few common structures include:

Deed of Trust with Promissory Note

The buyer receives title at closing, while the seller keeps a lien securing repayment.Vendor’s lien arrangement

The seller reserves lien rights in the sale documents to secure the unpaid balance.Contract for deed

The buyer often gets possession before receiving legal title, which creates more risk and more room for disputes.

If you’re trying to understand one of the riskier models, this article on how contract for deed work gives a useful starting point.

A home purchase should never leave the buyer confused about whether they own the property, and it should never leave the seller confused about how default will be enforced.

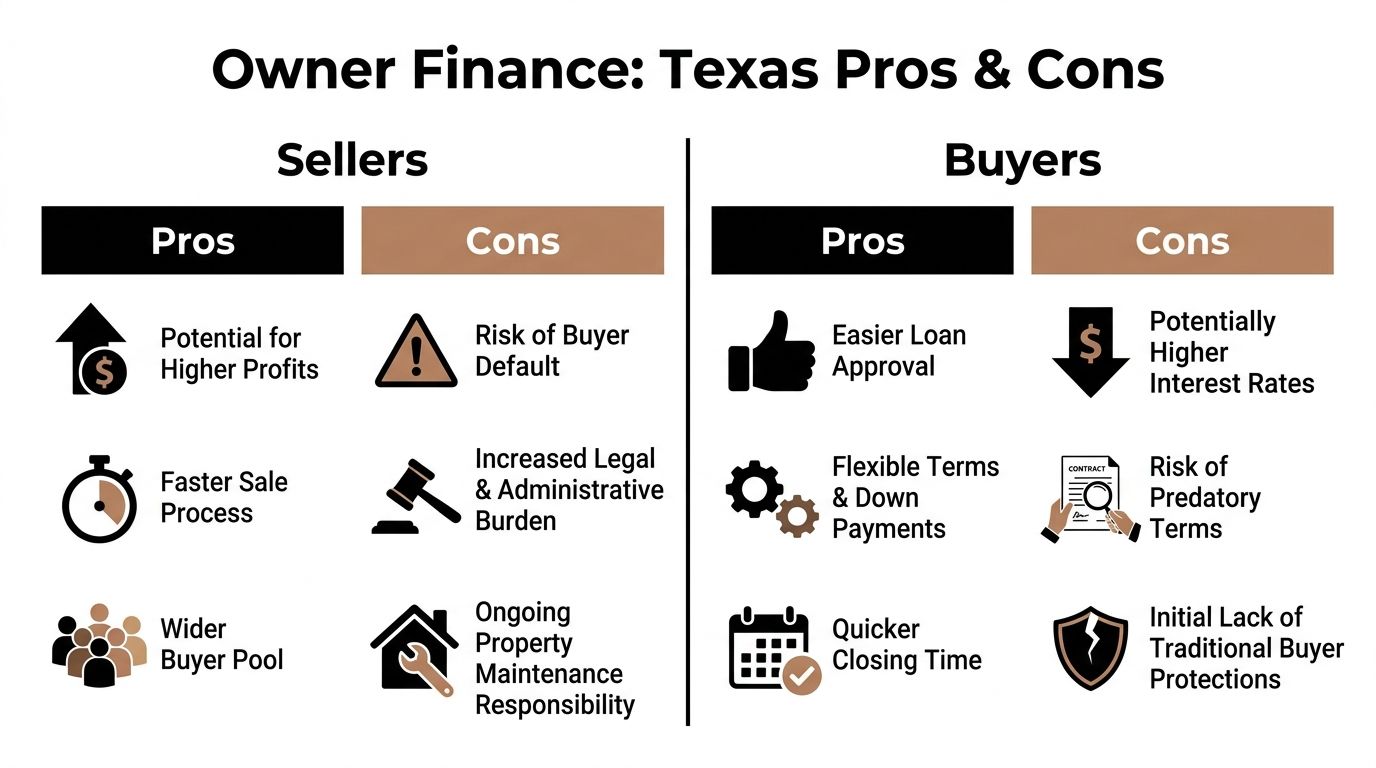

Pros and Cons for Texas Buyers and Sellers

Texas remains a strong market for nontraditional deal structures. The Texas REALTORS homebuyer and homeseller report shows that 82% of buyers nationally and 84% in Texas view a home purchase as a good investment, and first-time buyers in Texas financed a median of 91% of the purchase price, with down payments often coming from savings (52%) or proceeds from a prior home sale (34%) according to the 2023 Texas Homebuyer and Homeseller Report.

That helps explain why owner financing appeals to both sides. Buyers want access. Sellers want flexibility and control.

Why buyers consider it

For buyers, the biggest benefit is often simple. A seller may approve a deal that a bank will not.

That doesn’t mean the buyer should accept any terms offered. It means the buyer has room to negotiate around real circumstances.

Some buyer advantages are straightforward:

Flexible qualification

A seller may focus more on practical payment ability than a bank’s rigid underwriting model.Negotiable terms

Down payment size, payment timing, cure periods, repair obligations, and payoff terms are often open for discussion.Faster possession

When the parties are aligned and documents are ready, these deals can move more quickly than conventional financing.

Where buyers get hurt

The danger for buyers is assuming flexibility means safety.

A buyer in an owner-financed home may face:

| Buyer issue | Why it matters |

|---|---|

| Higher borrowing cost | The seller may charge more than a conventional mortgage lender would |

| Weak paperwork | Unclear title, vague default terms, or missing disclosures can create major risk |

| Harsh default consequences | A missed payment can trigger foreclosure rights or occupancy disputes |

| Limited institutional review | No bank is forcing appraisals, underwriting discipline, or closing compliance checks |

A buyer should also pay attention to insurance, tax escrow, maintenance duties, and whether any balloon feature or refinance expectation is realistic. If the contract assumes a later refinance that never happens, the buyer can end up boxed in.

Why sellers like these deals

Sellers usually like owner financing for business reasons.

They may be able to:

- Reach more buyers who can’t get a conventional loan

- Receive monthly income instead of a one-time payout

- Control terms instead of handing the process over to a mortgage lender

For some landlords, selling on terms can feel more attractive than continuing to manage tenants, repairs, and turnover.

Client-side reality: The benefits are real, but sellers often underestimate the paperwork and enforcement burden that comes with becoming the lender.

What sellers often underestimate

The seller’s risk starts after closing, not before it.

Common seller problems include:

Default management

If the buyer stops paying, the seller must enforce the agreement correctly.Document mistakes

Poor drafting can blur whether the occupant is a buyer, tenant, or something in between.Property condition issues

If the agreement doesn’t clearly assign maintenance responsibility, disputes start fast.Title and lien complications

Existing mortgages, tax issues, or recording errors can undermine the deal.

The best owner financing arrangements are not casual. They are carefully documented credit transactions with clear remedies and a realistic payment structure. If either side is relying on optimism instead of precise drafting, that’s usually where the deal starts to fail.

Essential Legal Documents in an Owner Financed Deal

The paperwork in an owner-financed home sale does more than “memorialize the deal.” It decides who owns the property, who has lien rights, what counts as default, and what legal process follows if the buyer stops paying.

That’s why document choice matters so much in Texas.

The promissory note

The promissory note is the buyer’s written promise to repay the debt.

It usually spells out the principal balance, interest, payment schedule, late charges if any, default terms, and what happens if the full balance is accelerated. If there is confusion later, lawyers and courts will go straight to this document.

A vague note creates expensive arguments. A strong note is specific about dates, payment method, grace periods, insurance obligations, tax handling, attorney’s fees, and what conduct counts as a breach.

The deed and security instrument

In many better-structured transactions, the buyer receives title at closing and the seller receives lien protection through the security documents.

That setup often includes a deed of trust, which secures the seller’s right to enforce the unpaid debt against the property. In Texas, that matters because a deed of trust can support non-judicial foreclosure when drafted and handled correctly.

The deed transferring ownership also matters. If you need a plain-English explanation of title transfer basics, this overview of a warranty deed in Texas helps show why deed language matters at closing.

Contract for deed and why it creates more risk

A contract for deed often delays title transfer until the buyer finishes paying the contract balance. That may sound attractive to sellers because they keep legal title longer, but it often creates more instability.

The buyer may be living in the home, paying taxes, making repairs, and acting like an owner while still lacking recorded title. If the relationship sours, the parties can end up fighting over whether the dispute is about title, possession, forfeiture, foreclosure, or eviction.

That is where many preventable problems begin.

A practical contrast

| Document | What it does | Main concern |

|---|---|---|

| Promissory note | Creates the repayment obligation | Bad terms cause payment disputes |

| Deed of trust | Secures the debt with the property | Enforcement must follow Texas law |

| Contract for deed | Delays title transfer until payoff | Possession and ownership can become blurred |

The safest deal is usually the one that answers the ugly questions before anyone signs. Who has title. Who pays taxes. Who insures the house. What notice is required. What process applies after default.

What should be written clearly

Every owner-financed home deal should define key obligations in plain English. At a minimum, the documents should address:

- Payment details including due date, place of payment, and what triggers default

- Insurance duties naming who must keep hazard coverage in place

- Tax responsibilities and whether escrow is used

- Repair allocation so routine maintenance and major system failures are not left open

- Possession rights including what happens if the buyer falls behind

- Remedies for default, cure rights, fees, and removal procedure

When documents are borrowed from a land deal, copied from the internet, or patched together from old forms, the risk climbs quickly. Residential transactions need drafting that matches the facts on the ground.

Navigating Texas Legal and Regulatory Requirements

Owner financing in Texas is regulated. It is not a private shortcut around lending law.

That matters most for sellers, because many assume they can carry the note with minimal paperwork. On residential property, that assumption can trigger serious liability.

Dodd-Frank ability to repay rules

Federal law requires sellers in qualifying owner-financed deals to evaluate whether the buyer can repay the loan. According to this explanation of Texas seller-finance compliance under the Dodd-Frank rules, the seller must review eight key factors, including the buyer’s income, assets, employment status, credit history, mortgage-related expenses, other debts, and debt-to-income picture.

The same source explains that non-compliance can expose the seller to buyer rescission rights for up to three years and civil penalties up to $500,000 per violation.

That is not a technicality. It’s a major risk point.

What sellers should actually collect

If a seller is financing a Texas home, the file should support the repayment decision with real documentation.

That commonly means gathering and reviewing:

- Income records such as pay stubs or tax returns

- Asset information that shows available reserves

- Employment verification where appropriate

- Credit information to understand existing obligations

- Debt details including recurring payments that affect affordability

- Housing cost projections including taxes and insurance

A seller who skips this step may think they are being flexible. Legally, they may be creating a challenge to the deal itself.

Compliance point: “I know this buyer and trust them” is not a substitute for documented ability-to-repay review.

Texas-specific issues sellers overlook

Texas adds its own layer of regulation and practical risk.

A few recurring issues include:

| Issue | Why it matters in Texas |

|---|---|

| SAFE Act licensing | Sellers financing more than five homes annually may need a mortgage loan originator license under Texas law |

| Usury limits | The contract interest rate must stay within legal limits |

| Balloon restrictions | Some loan structures create compliance and enforceability problems |

| Disclosure quality | Residential buyers need clear notice of obligations and default consequences |

Texas law also gives real weight to how a lien is documented and recorded. If a seller wants reliable enforcement rights, the structure cannot be vague.

Texas Property Code concerns after closing

Owner financing involves aspects typically handled by a Texas landlord tenant lawyer or eviction attorney.

If the contract is sloppy, a post-default dispute may stop looking like a clean secured transaction and start looking like a possession fight under the Texas Property Code. That creates confusion over notices, occupancy status, and whether the seller must pursue foreclosure, eviction, or both in sequence.

Texas Property Code provisions matter because possession rights often turn on the written agreement, the notices given, and whether the buyer’s status changed after default. The legal answer depends on the paper trail, not what the parties thought they agreed to.

A seller should never rely on oral promises. A buyer should never sign a home contract without understanding the enforcement mechanism. On residential property, compliance is part of the deal, not a side issue.

Common Pitfalls and How to Protect Your Rights

The biggest mistake people make with an owner-financed home is assuming default works like a simple missed payment on a private note.

It doesn’t. Once someone is living in the property, Texas possession law becomes part of the problem.

A major risk in owner-financed homes is the overlap with landlord-tenant law. According to this review of Texas owner-finance risks and dispute patterns on LandWatch, a defaulting buyer can become a tenant-at-sufferance, subject to eviction under Texas Property Code Section 24.005, and Texas courts saw a 15% rise in property contract disputes in 2025, many involving badly structured owner-financed home deals.

When default turns into a possession fight

A deed of trust default is one thing. An occupied house is another.

If the contract says the buyer becomes a tenant-at-sufferance after default, the seller may try to remove the occupant through an eviction path after giving the required notice under Texas Property Code Section 24.005. That process is technical. If the notices are wrong or the contract language is weak, the seller can face delay or a wrongful eviction claim.

For buyers, in owner finance, confusion becomes dangerous. Many believe they are only dealing with a loan issue, when they are also facing possible loss of possession.

What Texas Property Code means here

A few Texas Property Code concepts matter a lot in these disputes:

Section 24.005 notice rules

This section governs notice to vacate in eviction matters. If the occupant is being treated as a tenant-at-sufferance, notice compliance matters.Section 92.001 and related landlord-tenant principles

These provisions shape residential rights and obligations in ways that can become relevant when a seller tries to use lease-like remedies.Section 92.0081 concerns

Wrongful lockouts or improper self-help actions can create serious trouble for a seller trying to regain control too aggressively.

No seller should shut off utilities, change locks unlawfully, remove belongings, or rely on pressure tactics. No buyer should ignore formal notices assuming they are invalid just because the deal started as a sale.

Problems that show up before the default

Many owner-finance disputes begin with side issues that were never handled well in writing.

Common examples include:

Insurance lapse

The buyer was supposed to maintain coverage but didn’t. A storm hits, and now everyone argues over loss and repair responsibility.Unpaid property taxes

The contract says the buyer pays them directly, but no one verifies payment.Due-on-sale clause risk

If the seller still has an underlying mortgage, transferring the property can create a separate lender issue.Repair disputes

The air conditioning fails. The roof leaks. The contract never clearly assigned responsibility.

This is also where title issues can surface. If ownership history or lien priority is disputed, a court may need to sort out who holds enforceable rights. In some cases, a quiet title action becomes part of the larger fight.

Here’s a useful overview video on default and property disputes that often overlap with these issues:

How both sides protect themselves

Protection starts before signing, not after the first missed payment.

For sellers:

- Use documents drafted for a residential Texas home, not recycled land forms.

- Verify ability to repay and keep records.

- Define post-default possession status clearly.

- Follow notice rules exactly.

- Use court process. Never self-help.

For buyers:

- Confirm title status before closing

- Read the default section closely

- Understand whether you get title at closing

- Keep proof of every payment

- Respond quickly to notices

If the agreement blurs the line between buyer and tenant, a judge may end up deciding what the parties should have settled on paper at the start.

Is Owner Financing the Right Choice for You

Owner financing can solve a real problem. It can also create a bigger one if the parties treat it casually.

For the right buyer, it can provide access to a home that a conventional lender won’t finance. For the right seller, it can create monthly income and open the deal to a larger pool of buyers. Those are valid reasons to consider it.

But the decision should turn on structure, not enthusiasm.

When it may make sense

This route can be worth serious consideration when:

- The buyer has repayment ability but can’t fit a standard underwriting box

- The seller is prepared to act like a lender, not just a motivated owner

- The title is clean and reviewable

- The documents clearly define default, notice, and possession rights

- Both sides are willing to document everything properly

When caution should go up

Some situations call for extra care or a hard stop.

Be cautious if:

- The seller still has a mortgage and hasn’t addressed lender issues

- The contract delays title without giving the buyer meaningful protection

- The paperwork is homemade or copied

- The parties are relying on trust instead of clear remedies

- Nobody has evaluated how Texas Property Code rules apply after default

The trend line shows why this matters. Amid the Texas affordability crunch, owner-financed listings for improved properties reportedly saw a 28% increase, and the same source states that 22% of 2025 complaints involved residential owner-financed defaults that led to wrongful eviction suits under Property Code §92.0081, according to Land.com’s Texas owner-financing trend summary.

That doesn’t mean owner financing is a bad idea. It means sloppy owner financing is a bad idea.

The practical bottom line

A good owner-financed transaction is built like a serious real estate closing, because that’s what it is.

If you’re a buyer, protect your ownership path and possession rights. If you’re a seller, protect enforceability and compliance. If you’re already in a dispute, don’t assume the issue is only about missed payments. It may also involve title, notices, eviction procedure, and your rights under the Texas Property Code.

The most expensive version of owner financing is the one done cheaply at the start.

If you need help with an owner-financed home dispute, an eviction issue, lease confusion, or questions about your rights under the Texas Property Code, contact The Law Office of Bryan Fagan, PLLC for a free consultation today. Whether you need a Texas landlord tenant lawyer, guidance on tenant rights, or an eviction attorney to act quickly, the firm helps Texans protect their homes, contracts, and property rights with clear, practical advice.