Dealing with a landlord dispute or eviction can be stressful — but understanding your rights under Texas law can make all the difference. One of the first questions we hear from worried tenants is: "Will this ruin my credit?"

Here’s the straight answer: the eviction lawsuit itself won’t show up on your main credit reports from Equifax, Experian, or TransUnion. But that's only half the story. The financial fallout from an eviction can absolutely wreck your credit.

What the Texas Property Code Says About Evictions and Your Credit

Many tenants panic when they get an eviction notice, thinking the court filing immediately gets stamped onto their credit history. The truth is a little more complicated than that.

While the eviction is a public court record, it doesn't automatically land on your credit file. The real danger comes from any money the landlord claims you owe.

This could include:

- Unpaid rent

- Late fees

- Court costs

- Charges for alleged property damage

If you don't pay what the landlord says you owe, they can—and often will—sell that debt to a collection agency. That’s when the damage happens. A collection account is a huge red flag on your credit report.

It’s a common myth that an eviction has no impact on credit reports anymore. While it’s true the big three credit bureaus stopped including eviction judgments in 2017, that change doesn't protect you. The unpaid rent and fees are what really matter, and those debts are still reported by collection agencies.

This distinction is critical. A single collection account can tank your credit score and stay on your report for up to seven years. It makes getting a future apartment, a car loan, or even a credit card incredibly difficult.

For Texas renters, this means you can’t just move out and hope the problem goes away. Even if you leave, any outstanding debt can follow you for years, creating a serious financial roadblock. An experienced eviction attorney can help you navigate this process and protect your financial future. Read more about the findings on how eviction-related debts impact credit reports to see just how serious the consequences can be.

How Unpaid Rent Becomes A Credit Report Nightmare

It’s a situation no Texas tenant ever wants to face, but it happens more often than you’d think. A single late rent payment can quickly snowball, turning a simple landlord dispute into a financial nightmare that follows you for years. The path from a missed payment to a black mark on your credit report is a domino effect, and it’s critical to understand how one step leads to the next.

Let's walk through a common scenario. Say a tenant in Houston loses their job and falls behind. The unpaid rent and late fees add up to $3,000. Despite trying to work something out, the landlord decides to start the eviction process to get the property back.

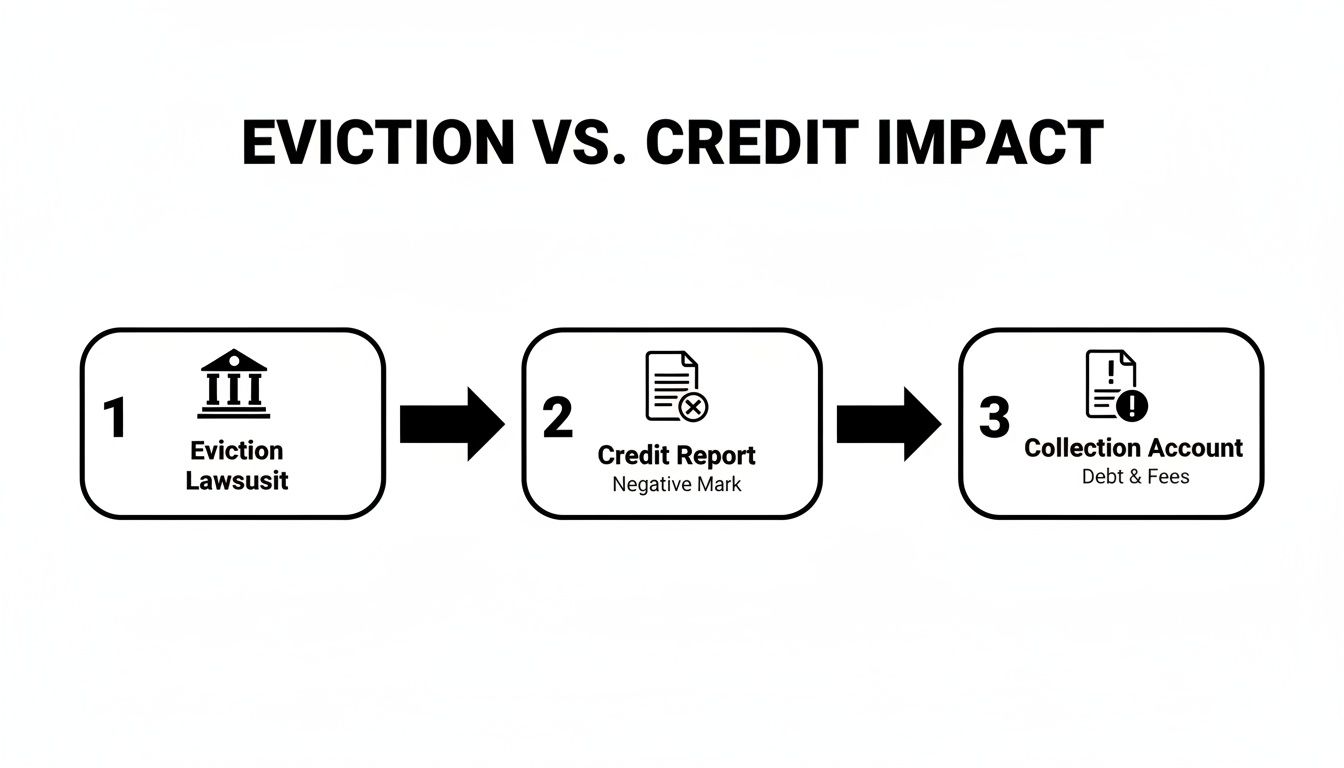

From Eviction Lawsuit to Monetary Judgment

Under the Texas Property Code, a landlord can sue a tenant for two things at once: possession of the property (the eviction itself) and any money owed under the lease. This is all handled in the same lawsuit, usually filed in a Justice of the Peace court.

If the judge rules in the landlord’s favor, they won’t just grant the eviction. They’ll also issue a monetary judgment for the $3,000 you owe. This is a court order, a legal document that officially says you are responsible for that debt. While the eviction order itself doesn't land on your credit report, this monetary judgment is the key that opens the door.

The Debt Collection Process

Most landlords aren’t in the business of chasing down old debts. It takes time and resources they just don't have. So, what do they do? They often sell the debt to a third-party collection agency, sometimes for just pennies on the dollar. The landlord gets a little money back, and the collection agency takes over the job of getting the full amount from you.

This is the moment your credit score takes a direct hit. The collection agency will report the unpaid debt to the big three credit bureaus—Equifax, Experian, and TransUnion.

The flowchart below breaks down how that eviction lawsuit indirectly creates a damaging collection account on your credit report.

As you can see, the eviction lawsuit itself stays in the court system, but the unpaid debt it legally confirms is what gets reported by collectors.

A collection account is a record of a debt that's been turned over to a collection agency. It's one of the most serious negative marks you can have on a credit report because it tells future lenders you didn't pay a past debt as agreed.

The damage can be severe. A single collection account can drop your credit score by 50 to 100 points, depending on what your credit looked like before. That negative mark will haunt your credit report for up to seven years, making it incredibly difficult to get approved for:

- Future apartment leases

- A mortgage or car loan

- New credit cards

- Even certain jobs

A simple dispute over rent is now a long-term financial burden. The eviction is just the start; the unresolved debt creates a ripple effect that can slam the door on your housing and financial options for years. To understand the legal steps in more detail, take a look at our guide on the eviction process in Texas. Knowing this timeline is the first step in protecting yourself from the damage.

The Hidden Report That Blocks Your Next Apartment

So you’ve managed to keep a collection account off your credit report. You might breathe a sigh of relief, thinking you’re in the clear. But when it comes to finding your next home, there's another report out there—one most tenants don't even know exists—that can kill your application before it's even read.

This is the world of tenant screening reports. And they tell a much, much different story about your history as a renter.

These specialized reports are completely separate from your files with Experian, Equifax, or TransUnion. While they’re governed by the same federal law—the Fair Credit Reporting Act (FCRA)—they’re built by different companies and packed with information designed specifically for landlords.

What Is on a Tenant Screening Report?

A standard credit report is all about your relationship with lenders. It shows your debts and payment history. A tenant screening report, on the other hand, digs into your life as a renter. Landlords use these to size up the risk of a new tenant, and what they see is often the final word on your application.

These reports pull from a different set of sources, revealing information your credit report misses entirely.

Credit Report vs Tenant Screening Report What Landlords See

To a landlord, your standard credit report is only half the story. The tenant screening report fills in the critical gaps they really care about. Here’s a look at what each one typically shows.

| Information Type | Shows on Standard Credit Report? | Shows on Tenant Screening Report? |

|---|---|---|

| Eviction Filings & Judgments | No, only if it results in a collection | Yes, filings and final judgments |

| Rental Payment History | Rarely, unless reported to bureaus | Yes, often reported by landlords |

| Credit Score & Debt History | Yes | Yes, usually included or pulled |

| Criminal Record | No | Yes, a key component |

| Public Civil Records | No | Yes, includes other lawsuits |

As you can see, the tenant screening report is far more revealing about your history as a renter. This is why an eviction filing—not just a judgment—can become such a massive problem. These comprehensive checks give landlords a deep look into a potential tenant's background. Understanding how an online background check works can give you a better idea of just how much information is being accessed during the screening process.

The most critical takeaway is this: an eviction filing can appear on your tenant screening report even if you won the case, the case was dismissed, or you settled with the landlord. The public record of the filing itself is enough to create a major roadblock for future housing.

A Dallas Tenant’s Nightmare Scenario

Think about this all-too-common situation in Texas. A tenant in Dallas gets an eviction lawsuit filed against them by their landlord over a repair dispute. The tenant knows their rights under the Texas Property Code, hires an attorney, and gets the case thrown out in court.

They feel victorious. They dodged an eviction and owe no money.

But a month later, they apply for a new apartment and get denied. Confused, they try another, only to be rejected again. The problem? That eviction filing, despite the dismissal, is now a black mark on their tenant screening report. To a prospective landlord, the "dismissed" status doesn't matter; they just see the red flag of an "eviction" record and immediately move on.

This single filing can haunt a tenant screening report for up to seven years. The scale of this is staggering. In the last year alone, roughly 1.1 million eviction filings were recorded across just 10 states and 34 cities, with Texas courts handling a huge chunk of that volume.

For a Texas renter, this means one dispute can threaten your housing stability for years, no matter how it ended. It’s why avoiding a filing in the first place is every bit as important as protecting your credit score. You can read more about the far-reaching impact of evictions on housing stability to see how this plays out nationwide. For landlords, understanding these long-term consequences should be a powerful incentive to resolve disputes before running to the courthouse.

Know Your Rights Under Texas Law And The FCRA

Facing an eviction or a heated dispute with your landlord is overwhelming. It feels like your entire financial future is on the line—because it is. But you aren't powerless. Understanding your rights is the first step in fighting back against lasting damage to your finances and ability to rent again.

Your strongest shields in this fight are the Texas Property Code and the federal Fair Credit Reporting Act (FCRA). Together, they give you a legal framework to defend yourself, but you have to know how to use them.

Your Protections Under The Texas Property Code

In Texas, a landlord can’t just decide to kick you out on a whim. The law lays out a very specific, non-negotiable process they must follow, starting with the “Notice to Vacate.”

Under Section 24.005 of the Texas Property Code, if you fall behind on rent, your landlord is required to give you a written notice with at least a three-day warning before they can legally file an eviction lawsuit. This isn't just a courtesy; it's the law. If they just send a text, call you, or don't wait the full three days, the entire eviction filing could be thrown out.

This is your first—and most critical—line of defense. It gives you a brief but vital window to pay the rent, negotiate a solution, or call a tenant rights lawyer before that damaging eviction case ever sees the inside of a courtroom.

Using The Fair Credit Reporting Act (FCRA) to Your Advantage

While Texas law controls the eviction process itself, the FCRA is what governs your credit and tenant screening reports. This is the federal law that gives you the power to see what’s being said about you—and, more importantly, to fight back when it's wrong.

The FCRA is the reason you don’t have to just accept an error that costs you a new home. It’s designed to ensure fairness and accuracy in the information landlords and lenders use to judge you.

Under the FCRA, you have an absolute right to an accurate report. If a collection agency is still reporting a debt you paid off, or a screening company lists an eviction that was dismissed, you have the legal right to demand they fix it.

This is where keeping your own records becomes a game-changer. Good documentation is the ammunition you need to win a dispute.

Step-by-Step Guide to Checking and Disputing Your Reports

Don't wait for a rejection letter from a new apartment to find out there's a problem. You have to be proactive. Here’s how you can get ahead of it and take control.

- Pull Your Reports: You can get a free credit report from the big three bureaus (Equifax, Experian, TransUnion) every single year at AnnualCreditReport.com. You can also get copies of your tenant screening reports, though you may have to ask a potential landlord which service they use to know who to contact.

- Scan for Errors: Go through every single line. Are there collection accounts for debts you've settled? Incorrect balances? Eviction records that were dismissed or shouldn't be there at all?

- Gather Your Proof: This is where your hard work pays off. Pull together everything that proves your case—payment receipts, bank statements, emails from your landlord confirming payment, or court orders showing an eviction was dismissed.

- File a Formal Dispute: Send a written dispute letter to the credit bureau and the company that reported the bad information (like a collection agency). Clearly explain the mistake and include copies (never originals!) of your proof. By law, they have to investigate your claim, usually within 30 days.

If your dispute is successful, the negative mark must be removed. By knowing these rules, you can stop being a victim of the system and start managing your own rental and financial future. Our team can help you understand the specific protections available under the Texas Property Code for tenant rights and turn that knowledge into action.

How to Clean Up Your Record After An Eviction

An eviction on your record feels like a permanent black mark, a life sentence for renting. Finding out that old eviction is shutting doors to new housing is crushing, but you have more control than you realize. With the right strategy, you can clean up your record and move forward.

Even if that negative mark is already there, you can take powerful, practical steps to repair the damage. It takes work and a clear plan, but overcoming the fallout from an eviction is absolutely possible.

Step 1: Negotiate a Pay-for-Delete Agreement

If the eviction landed a collection account on your credit report, one of your best moves is negotiating a “pay-for-delete” agreement. It’s exactly what it sounds like: you pay an agreed-upon amount of the debt, and in exchange, the collection agency completely removes the account from your credit reports.

Here’s the game plan:

- Get in Touch: Call the collection agency and tell them you want to settle the debt, but only if they agree to delete it from your credit file.

- Negotiate the Price: You can almost always settle for less than the full balance. Start low and be ready to go back and forth.

- Get It in Writing: This is the most critical step. Do not pay a single dollar until you have a signed, written agreement from the agency confirming they will delete the account after your payment. A verbal promise means nothing.

Once you’ve paid per the agreement, keep a close eye on your credit reports to make sure they held up their end of the bargain. This one move can give your credit score a serious boost and wipe a major red flag off your record.

Step 2: Seal the Public Eviction Record in Texas

Even with a clean credit report, the public court record of the eviction filing can still show up on tenant screening reports and kill your application. In Texas, you might be able to get this record sealed through a legal process called an expunction or an order of nondisclosure.

But sealing an eviction record isn’t automatic. You usually have to meet specific criteria to petition the court. You may have a shot if:

- The judge ruled in your favor: If you won the case, you have a strong argument for getting the record sealed.

- The case was dismissed: If the landlord dropped the lawsuit or it was thrown out on a technicality, you can also ask the court to seal it.

Sealing the record makes it invisible to the public, which includes most tenant screening services. It effectively erases the eviction from view, giving you a real fresh start with future landlords.

The process means filing a formal petition in the same court that handled the eviction. The legal requirements are tricky, so working with a Texas tenant rights lawyer is your best bet to make sure it’s done right. If your eviction case resulted in records being posted online, learning how to remove court records from the internet is another key piece of the puzzle.

Step 3: Write a Compelling Letter of Explanation

What happens if you can't get the record removed? Sometimes the eviction judgment is valid, or a collection agency won't budge. When that’s the case, your best strategy is to own it with a well-written letter of explanation for potential landlords.

This isn’t an excuse letter. It's your chance to give context and prove you’re responsible. A good letter does three things:

- Acknowledge what happened: Be brief and honest. Did you lose your job? Face a medical emergency? Explain the temporary hardship that led to the eviction.

- Show you’ve fixed the problem: Detail the steps you've taken to make sure it never happens again. You've found a stable job, paid the old debt, or built an emergency fund.

- Provide solid references: Include letters from employers, previous landlords (if you have good ones), or others who can speak to your character and reliability.

By tackling the issue head-on, you prove you're transparent and have become a responsible tenant. Paired with an otherwise strong application, a sincere letter can be the thing that gets you approved. It's also vital to handle any related financial fallout, like a money judgment. To better understand how these orders work, you can review our guide on the Texas Abstract of Judgment.

A Landlord's Guide to Fair and Legal Collections

Chasing down unpaid rent is one of the most frustrating parts of being a landlord. You're running a business, and when a tenant leaves you with a significant debt, it puts your investment at risk. But going after that money must be done by the book, or you could end up in a legal fight that costs you more than the original debt.

Before you can even think about collections, you need an ironclad paper trail. This isn't just a suggestion; it's your first and most critical step. You need a perfect record of every missed payment, every late fee your lease allows for, and any court judgments you've won. Without it, you have nothing to stand on.

Following The Texas Property Code

The Texas Property Code isn't just for tenants—it lays out your responsibilities, too. The law demands you provide a formal, written "Notice to Vacate" before even starting the eviction process for non-payment of rent.

The same principle applies to collecting a debt. You are legally responsible for making sure the amount you report to a collection agency or credit bureau is 100% accurate. If you report the wrong amount or forget to update a debt that's been settled, the tables can turn, and you could be the one facing a lawsuit from your former tenant.

A word of caution: Never use debt collection to get even with a difficult tenant. Both the federal Fair Debt Collection Practices Act (FDCPA) and the Texas Debt Collection Act (TDCA) have strict rules against harassment or deceptive tactics. The goal is to recover what you're legitimately owed, not to punish someone.

Using a Third-Party Collection Agency

Handing the problem over to a professional collection agency can feel like a huge relief. It saves you time and headaches, but it doesn't wash your hands of the situation entirely.

- Pros: Collection agencies are specialists. They have the tools and know-how to track down former tenants and navigate the legal process, freeing you up to manage your properties.

- Cons: You'll pay for their service, usually a cut of whatever they recover. More importantly, if the agency you hire breaks the law or harasses the tenant, you can still be held liable.

Remember, whenever you're handling tenant data for reporting or screening, you're also operating under the Fair Credit Reporting Act (FCRA). That means keeping data accurate and secure is your job. Sticking to these guidelines is the best way to protect your bottom line while staying on the right side of the law.

Straight Answers to Your Toughest Questions About Evictions and Credit

When you’re caught in a landlord dispute, the uncertainty can be overwhelming. You're not just worried about where you'll live—you're worried about your credit, your finances, and what this all means for your future.

Let’s cut through the confusion. Here are clear, straightforward answers to the questions we hear most often from Texas tenants and landlords.

How long does an eviction stay on your record?

This is a tricky question because there isn't just one "record." It really depends on which document you're talking about.

A collection account tied to unpaid rent or damages can linger on your standard credit report for up to seven years. But the court record of the eviction filing itself is a different story. That public record can show up on specialized tenant screening reports for just as long—up to seven years—even if you won the case or it was dismissed.

Can my landlord report me for breaking a lease?

No, not directly. A landlord can’t just call up the credit bureaus and report that you broke your lease. That’s not how it works.

What they can do is pursue you for money owed. If breaking the lease leaves you with a debt for unpaid rent or fees, the landlord can hand that debt over to a collection agency. It's the collection agency that will report the unpaid account to the credit bureaus, causing it to appear on your credit report.

What should I do if my landlord threatens eviction?

First, don't panic. A threat is not a legal eviction. Your landlord can't just throw you out.

Your first move should be to pull out your lease and review your rights under the Texas Property Code. Do not move out just because your landlord told you to. Keep a written record of every conversation, text, and email. Most importantly, talk to a Texas landlord tenant lawyer to figure out your next steps. The law requires your landlord to follow a very specific legal process to remove you.

Important: It is illegal for a landlord to take matters into their own hands. They cannot change the locks, remove your belongings, or shut off your utilities to force you out without a formal court order. These are considered illegal "self-help" evictions.

Does paying the debt remove the eviction judgment?

Paying off the money you owe satisfies the financial part of the judgment, but it does not make the eviction disappear from public records.

The judgment itself—the court's official decision—will still exist. It can continue to pop up on tenant screening reports for years unless you take the next step and successfully petition the court to have the record sealed or expunged.

If you need help with an eviction, lease issue, or rental dispute, contact The Law Office of Bryan Fagan, PLLC for a free consultation today.