Dealing with a property deal outside a normal bank loan can feel risky fast. Many Texans start looking at owner financing because a lender said no, the property has issues, or the seller wants a quicker path to closing. The appeal is obvious. The danger usually isn't.

The part many people miss is that an owner-financed sale doesn't stay neatly inside real estate law. In Texas, it can slide into the same practical world as lease disputes, possession fights, default notices, and even eviction court. If you're a buyer, you need to know what rights you're getting. If you're a seller, you need to know what remedies you're creating.

This owner finance definition guide explains the deal in plain English, then connects it to the Texas Property Code, tenant rights, and the kind of disputes that land people in front of a judge.

What Is Owner Financing in Texas?

Owner financing means the seller finances the sale instead of a bank. In plain terms, the seller acts like the lender. You agree on a purchase price, a down payment, an interest rate, a payment schedule, and what happens if the buyer stops paying.

That simple definition matters because many people confuse owner financing with renting, a lease-option, or an informal payment plan. It isn't any of those by default. It's a real sale structure. The legal paperwork decides whether the buyer is functioning like an owner, a borrower, a tenant, or some uneasy mix of all three.

The seller becomes the bank

In a traditional mortgage, a bank wires the money and the buyer repays the bank over time. In owner financing, the seller extends credit directly to the buyer. That arrangement can help when a buyer has credit trouble, nontraditional income, or needs terms a bank won't offer.

Owner financing isn't rare or fringe. In 2017, seller financing produced 89,779 first-position notes on residential properties totaling $17.3 billion, with average loan sizes rising 12% to $184,992. Nearly $8 billion of these notes targeted residential properties, according to 2017 seller financing statistics.

Practical rule: If someone says, "We'll just work it out between ourselves," slow down. If the seller is acting as the lender, you need real loan documents and a Texas-compliant contract.

Why Texans look at it

Some buyers use owner financing because they can't get approved through ordinary underwriting. Some sellers use it because they want monthly payments, a quicker closing, or flexibility on terms. In Texas, it's also common to see owner financing discussed alongside contracts for deed, land contracts, and other creative sale structures.

The owner finance definition that matters most is this: a property sale with seller-provided credit, backed by legal documents that control possession, title, default, and remedies.

That last part is where the risk lives. In Texas, the contract language can decide whether a payment problem becomes a foreclosure fight, a possession case, or something that looks a lot like landlord-tenant litigation.

How an Owner Finance Agreement Works

An owner finance deal usually starts with a basic business problem. The buyer wants the property but can't or won't use a conventional lender. The seller is willing to carry the debt if the risk is controlled.

The core paperwork usually includes a promissory note and security documents. If you want a simple reference for how promissory notes are commonly structured, that overview helps explain the basic lending terms people often overlook.

The key documents

The promissory note is the buyer's written promise to repay. It should spell out the principal balance, interest rate, due dates, late-payment rules, default terms, and any balloon payment.

The security instrument, often a deed of trust in Texas practice, gives the seller a way to enforce the debt if the buyer defaults. Without clear security language, a seller may have a note but weak remedies. Without clear note terms, a buyer may be exposed to vague defaults and surprise charges.

If you're comparing structures, this guide on how a contract for deed works in Texas helps show why form matters so much.

The money terms buyers and sellers usually see

In owner financing, the seller extends credit through a promissory note with terms like a 10% to 20% down payment, an interest rate between 6% and 10%, and a repayment schedule that often requires a full balloon payment after 5 to 10 years, according to Business Insider's explanation of owner financing. That same source notes that this structure can bypass traditional underwriting and may open the door for buyers with credit scores under 620.

Those numbers matter for both sides.

- Down payment matters first. A larger down payment lowers the seller's risk and shows the buyer has real money in the deal.

- Interest rate reflects risk. Seller-carried paper often costs more than a conventional loan because the seller is taking on lending risk directly.

- Short term creates pressure. A deal may feel affordable monthly but still end with a large amount due later.

If the monthly payment is the only number you're focused on, you're reading the wrong part of the contract.

A plain-English sequence

Buyer and seller agree on price and terms. This includes down payment, note amount, payment schedule, and what counts as default.

Closing documents are prepared. The buyer signs the note and the security documents. The deed, title issues, and recording details need close attention.

Buyer takes possession under the contract terms. Depending on the structure, that may happen with immediate ownership rights or with more limited rights.

Buyer makes monthly payments to the seller or a servicer. Good recordkeeping is critical.

The deal ends by payoff, refinance, sale, or default. That's where the fine print starts to control the outcome.

A clean deal works because the contract is precise. A messy deal falls apart because the parties treated a real estate loan like a handshake.

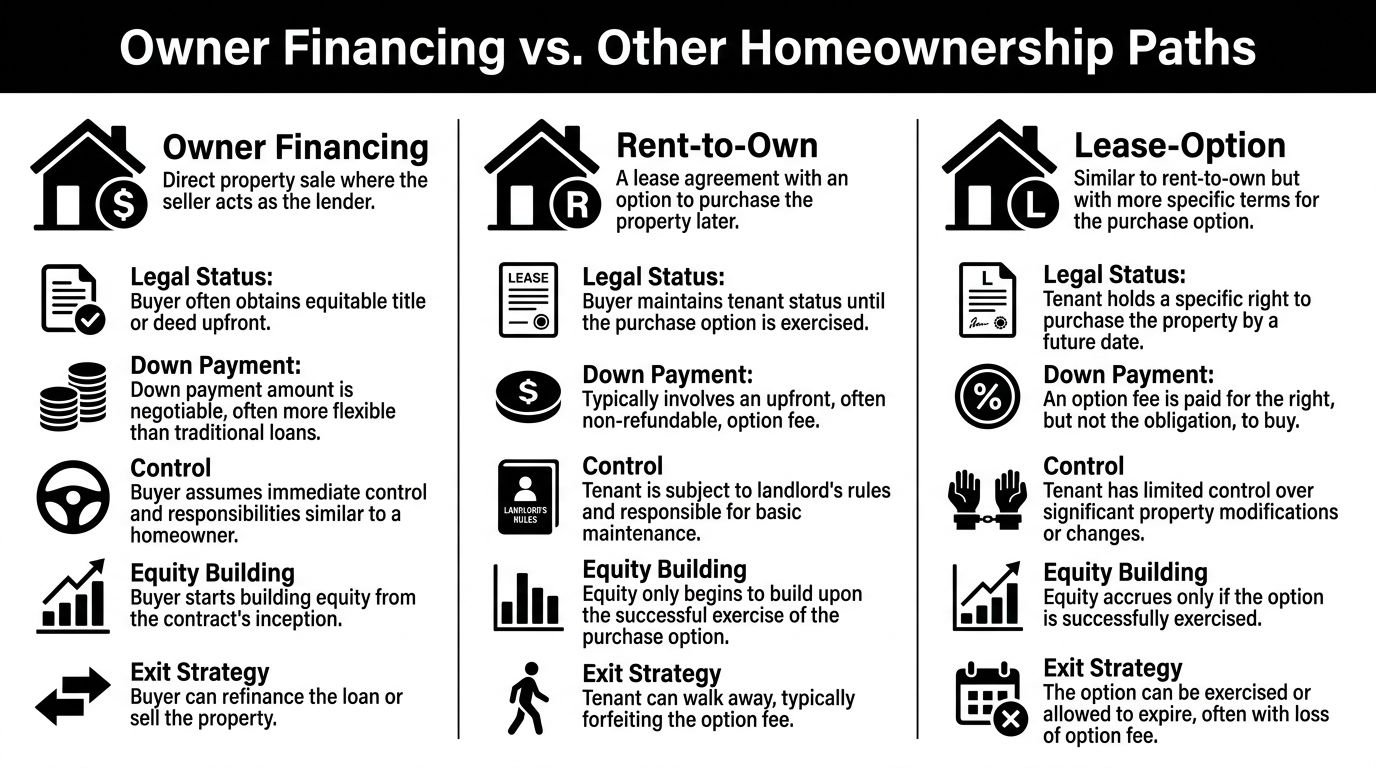

Owner Financing vs Rent-to-Own and Lease-Options

People often use these labels as if they mean the same thing. They don't. In Texas, the difference affects title, possession, equity, remedies, and whether your dispute may start sounding like a landlord-tenant case.

The biggest legal difference

With owner financing, the transaction is built as a sale with seller-provided credit. The buyer is not just renting and hoping to buy later. The contract usually treats the buyer as someone purchasing the property and paying the seller over time.

With rent-to-own or a lease-option, the occupant usually begins as a tenant. They lease the property first and may have the right, or in some structures the expected path, to purchase later. Until that option is exercised and the sale closes, their legal position may look much more like a renter than a buyer.

For a closer look at one of these hybrid structures, see this discussion of what a lease purchase contract is in Texas.

A side-by-side view

| Structure | Legal status at the start | Equity position | If payments stop |

|---|---|---|---|

| Owner financing | Buyer is entering a sale transaction financed by the seller | Buyer may build an ownership interest under the contract terms | The remedy depends heavily on how the documents are written |

| Rent-to-own | Occupant is usually a tenant first | Equity usually doesn't build like a true purchase until the option is exercised | Landlord remedies often matter early |

| Lease-option | Tenant has a contract right to buy later | The option may have value, but ownership usually waits until purchase | Missed lease payments can threaten both housing and the future purchase right |

Where people get hurt

The most common mistake is assuming any arrangement with monthly payments toward a house means "I'm basically the owner." That's not safe thinking in Texas. Your rights come from the signed documents, not the label people used in a conversation.

Consider these practical differences:

- Control of repairs: In a lease-style deal, repair duties may still track landlord-tenant expectations. In a sale-style deal, the buyer often carries more responsibility.

- Possession rights: A tenant usually has possession through a lease. A buyer under a financing arrangement may have possession tied to payment performance and contract compliance.

- Default consequences: Missing payments under a lease-option may trigger lease remedies. Missing payments under owner financing may trigger remedies that are even harsher if the paperwork is drafted badly.

A deal can look like homeownership on move-in day and feel like an eviction case by default day.

That is why the owner finance definition has to include legal status, not just payment method. If you don't know whether the contract makes you a buyer, borrower, tenant, or option holder, you don't yet understand the deal.

Legal Risks for Texas Buyers and Sellers

Owner financing can solve a financing problem. It can also create a litigation problem. Buyers usually focus on getting into the property. Sellers usually focus on getting the note signed and the down payment collected. Both can miss the risk that arrives later.

The balloon payment problem

A short-term note often feels manageable because the monthly payment is spread over a longer amortization idea, while the contract still matures much sooner. The trouble appears at the end.

According to Rate's owner financing overview, balloon payment mechanisms often require a terminal payment of 50% to 70% of the original principal after 5 to 10 years. That source gives an example of a $400,000 sale with a 7-year term that could leave a balloon payment of around $280,000, and it identifies failure to refinance as a primary cause of default.

For a buyer, that means years of steady payment may still end in crisis if refinancing isn't available when the balloon comes due.

Risks that hit buyers hard

A buyer in an owner-financed deal can run into trouble in several ways:

- Refinance failure: Credit, income, title issues, or market conditions can block the payoff plan.

- Unclear title problems: If the seller's own financing or title condition wasn't handled correctly, the buyer may inherit a legal mess.

- Default definitions that are too broad: Some contracts treat minor breaches like major defaults.

- Loss of bargaining power after move-in: Once you've invested money in repairs, moving feels harder even if the contract is bad.

Risks sellers often underestimate

Sellers face their own exposure.

- Enforcement costs: A defaulting buyer doesn't remove themselves just because payments stopped.

- Property condition issues: A buyer in distress may neglect the house before the dispute ends.

- Existing lender issues: If the seller still has debt on the property, sale terms may trigger conflicts with that lender.

- Bad drafting: A seller can think they have strong rights and learn too late that the paperwork is defective.

The contract should answer hard questions before anyone signs it. Who pays taxes, who carries insurance, what notice is required, and what remedy follows default.

What works and what doesn't

What works is a documented, fully reviewed transaction with title work, payment records, and default language tied to enforceable Texas remedies.

What doesn't work is a shortcut. A handwritten addendum, an internet form used without revision, or a deal built around trust instead of enforceable terms often creates the kind of dispute neither side expected.

Key Protections to Include in Your Contract

A strong owner finance contract doesn't try to sound overly complex. It answers the practical questions a judge would ask later. If the agreement is vague, the dispute gets expensive.

In Texas, the Texas Property Code is significant. Section 5 contains rules that often come into play in executory contracts and seller-financed residential transactions. Chapter 24 matters when possession becomes disputed. Section 92.001 and related landlord-tenant provisions can also become relevant when the parties start arguing about occupancy, notice, or whether the relationship has shifted into something that looks like a tenancy.

For background on drafting terms cleanly, this page on real estate contracts in Texas is a useful starting point.

Clauses that should never be vague

Use this checklist when reviewing a proposed deal:

- Exact payment terms: State the amount due, due date, grace rules, late fees if any, where payment goes, and how payments are credited.

- Balloon disclosure: If a large payoff comes later, the contract should say so plainly and in language no one can miss.

- Default definition: Spell out what counts as default. Missed payment, unpaid taxes, no insurance, unauthorized transfer, waste to the property, or other listed breaches.

- Notice and cure rights: Say how notice is delivered and how long the defaulting party has to fix the problem.

- Remedies: The contract should state what the seller can do if the buyer defaults and whether the process is foreclosure-based, forfeiture-based, or tied to possession rights under Texas law.

- Taxes and insurance: These obligations should never be left to assumption.

- Repair duties: Buyers and sellers fight over this constantly when the contract blurs the line between sale and occupancy.

Provisions that prevent later chaos

Some terms don't get enough attention until there's a dispute.

Title and lien disclosures

The buyer needs to know whether existing liens exist and how they affect the transaction.Recording and document handling

If a deed, deed of trust, or memorandum should be recorded, that process should be addressed clearly.Possession language

This is critical. The contract should explain whether the buyer has possession as an owner in possession, a contract purchaser, or under some separate occupancy arrangement.

Client warning: If your contract uses sale language in one paragraph and tenant language in another, stop and get it reviewed.

Why this matters in real life

The best contract doesn't just help the seller collect payments. It protects the buyer's investment and reduces the chance that a disagreement turns into a fast possession case. If you're searching for a Texas landlord tenant lawyer, an eviction attorney, or guidance on tenant rights under the Texas Property Code, this is exactly the overlap that deserves careful legal review before closing, not after default.

When a Bad Deal Becomes a Texas Eviction

This is the part many buyers never see coming. They believe that if they miss payments, the seller must file a long foreclosure case and sort out everyone's equity later. In some Texas owner finance disputes, that isn't how the fight starts.

A common pattern looks like this. A buyer moves into the home under an owner-financed arrangement, pays for a while, maybe improves the property, then falls behind. The seller points to the contract and says the buyer's right to stay in the property has ended. Now the dispute is no longer just about debt. It becomes a fight over possession.

According to this discussion of owner financing defaults in Texas, upon default in some owner finance deals, sellers can evict buyers through justice court under Chapter 24 of the Texas Property Code, rather than pursuing a costly judicial foreclosure. That source also warns that this can turn buyers into tenants and cause them to lose built-up equity. It further notes FTC warnings citing default rates as high as 30% in some markets, leading to "yo-yo sales" where sellers relist property after stripping the buyer's equity.

How the dispute shifts from sale to possession

Chapter 24 of the Texas Property Code governs eviction procedures, often called forcible detainer cases. Those cases are designed to decide who has the right to immediate possession. They are not built to resolve every title issue or every fairness argument about money already paid.

That creates a serious problem for buyers. If the contract gives the seller a path to treat the buyer's occupancy like a possession issue after default, the buyer may be defending a case on a much faster timeline than a typical foreclosure fight.

Here is the practical sequence many people don't anticipate:

- A payment is missed

- A default notice is sent

- The seller claims possession rights

- The case lands in justice court

- The buyer argues "I was purchasing the home," while the seller argues "you lost the right to stay"

If you're trying to understand the broader consequences of missed mortgage payments, it's helpful to compare those consequences with how much faster a possession dispute can move under the wrong owner-finance structure.

Why buyers and sellers both need counsel early

For buyers, the risk is obvious. You may lose the house and the money you already put into it.

For sellers, the risk is different but still serious. If your documents are sloppy, your notices are defective, or your remedy doesn't match Texas law, you can lose time, weaken your position, and invite counterclaims. That is especially true if the property condition, habitability complaints, or side agreements start making the case look like a landlord-tenant dispute.

This video gives more context on the legal issues surrounding these disputes.

The safest approach is simple. Treat owner financing like a high-stakes legal transaction from the first draft. Don't assume the label on the deal will protect you. In Texas, your rights often turn on the exact language used, the notices sent, and the remedy the contract allows.

If you need help reviewing an owner-finance deal, responding to a default notice, protecting tenant rights, or handling an eviction-related property dispute under the Texas Property Code, contact The Law Office of Bryan Fagan, PLLC for a free consultation today.