Dealing with a legal dispute can be stressful—but discovering a judgment has been placed against your property can feel overwhelming. Understanding your rights and the power of a Texas abstract of judgment can make all the difference in protecting your assets.

An abstract of judgment in Texas isn't just a piece of paper. It's a powerful legal tool that a creditor uses after winning a lawsuit to put a lien on your property. Think of it as a public, official claim against your real estate—one that secures the debt and makes it incredibly difficult for you to sell or refinance until you’ve settled up.

What To Do About a Judgment on Your Property

Discovering a judgment lien attached to your property can feel like a punch to the gut. This guide is here to cut through the confusion and give you clear, practical guidance to move forward.

This kind of lien usually pops up after a court case, like a dispute with a creditor or a former landlord, ends with a monetary award against you. The abstract itself isn't the lawsuit—it's the document that takes the court's private decision and makes it a public record attached directly to your real estate.

Your First Steps in Addressing a Judgment Lien

The moment you find out about a judgment lien, the clock starts ticking. This lien puts a "cloud" on your property's title, effectively blocking you from selling, refinancing, or in some cases, even transferring ownership until the debt is resolved. Ignoring it is the worst thing you can do, as interest keeps piling onto the original judgment amount.

Here is a step-by-step plan to get started:

- Step 1: Verify the Judgment. First things first, get the facts straight. Confirm every detail on the abstract—the creditor's name, the judgment date, and the total amount owed. You need to be sure it's valid and filed correctly.

- Step 2: Understand Its Impact. This lien doesn't just affect one property. It attaches to any non-exempt real estate you own in the county where it was filed.

- Step 3: Explore Your Legal Options. You're not stuck. Your options can range from paying the debt outright to negotiating a smaller settlement or, if there are grounds, challenging the lien's validity in court. A skilled Texas landlord tenant lawyer can help you determine the best path.

The process has a clear structure, much like handling other legal matters. Just as there are specific steps for how to appeal an eviction, there are defined procedures for dealing with a judgment lien.

Under Chapter 52 of the Texas Property Code, an abstract of judgment creates a lien that stays active for 10 years. The catch? Creditors can often renew it, potentially extending their claim on your property for much longer if the debt goes unpaid.

Navigating this corner of Texas property law demands a solid strategy. Whether you're a landlord who just won a judgment or a property owner now facing a lien, understanding your rights and responsibilities is the first step toward clearing your title and protecting your assets.

What the Texas Property Code Says About an Abstract of Judgment

When you're dealing with a legal battle, the terminology alone can feel overwhelming. Let’s clear up one of the most critical terms you might encounter: the Texas abstract of judgment.

This isn't the lawsuit itself. It’s the powerful document that comes after a court decides someone owes money.

Think of it as the tool that turns a judge's decision into real-world action. Its main job is to create a legal claim—called a lien—on any non-exempt real estate the debtor owns in the county where it’s filed. It’s like a creditor putting a temporary "hold" on the property's title, making sure they get paid if the owner tries to sell or refinance.

What Makes an Abstract of Judgment Valid?

For this document to have any legal teeth, it has to be perfect. The Texas Property Code § 52.002 lays out exactly what information must be included.

Even a small mistake can make the entire lien invalid. That’s why getting the details right is so crucial for both the person owed money (the creditor) and the person who owes it (the debtor). A detail-oriented eviction attorney will often review these documents for errors.

To get a better feel for this, checking out some expert tips on writing legal documents can provide serious insight into why every word matters. Precision isn't just a suggestion; it’s a legal requirement that protects everyone involved.

At its core, an abstract of judgment acts as a public notice. It officially converts a court's financial award into a real property lien, attaching the debt to any real estate the debtor owns in that county. This gives a creditor significant leverage, potentially tying up a property for up to ten years.

Key Components of a Texas Abstract of Judgement

Texas law is very specific about what must be on this form for it to be valid. Each piece of information serves a distinct legal purpose, ensuring the right person is held responsible for the right amount.

Here’s a look at what must be included.

| Information Required | Why It Is Important |

|---|---|

| Names of Plaintiff & Defendant | Clearly identifies the creditor (plaintiff) and the debtor (defendant) to avoid any confusion or mistaken identity. |

| Debtor's Birthdate & Address | Helps distinguish the debtor from others with a similar name and provides a last known address for legal notices. |

| Date and Amount of Judgement | Establishes the exact date the debt became official and the precise principal amount owed, which is crucial for calculating interest. |

| Court & Case Number | Links the abstract directly back to the specific court case that resulted in the judgment, ensuring a clear legal trail. |

| Credits Paid on the Judgement | Records any payments already made, ensuring the debtor is only liable for the remaining balance. |

If any of these critical details are missing or wrong, the lien could be challenged and possibly thrown out.

For property owners, double-checking these elements is your first line of defense. For creditors, getting them right is the only way to secure your claim. A valid abstract tells the world—especially title companies, lenders, and potential buyers—that a debt is tied to the property. Understanding these parts gives you the power to verify the document's legitimacy and protect your rights.

The Real-World Impact of a Judgement Lien

When a Texas abstract of judgment gets filed, it does a lot more than just put a debt on the books. It sets off a chain reaction of real-world consequences that can turn your life as a property owner upside down.

The most immediate effect? It slaps a judgement lien on your real estate, which effectively "clouds" your property's title.

This cloud is a serious problem. It’s a red flag to everyone—potential buyers, mortgage lenders, and title companies—that a creditor has a legal stake in your property. Until that claim is paid off, you’re basically stuck.

How a Lien Stops Property Sales and Refinancing Cold

Real-World Scenario: Imagine you've found the perfect buyer for your house. You’ve settled on a price, the contracts are signed, and you're just days away from closing. But then, the title company runs its routine check of public records and finds the judgment lien.

Suddenly, the brakes slam on the entire deal.

The title company can't issue a clear title policy to the new buyer, which is non-negotiable for nearly every real estate transaction. The sale is now on the verge of collapse, and you're left scrambling to deal with a debt you might have forgotten even existed. The same exact thing happens if you try to refinance your mortgage—no lender will approve a new loan on a property with an unresolved lien attached.

This kind of situation is incredibly stressful, not unlike getting an unexpected legal notice threatening to remove you from your home. Just as a tenant needs to understand the power behind a formal writ of possession in Texas, a property owner has to grasp the immense power a lien holds over their assets. Understanding your tenant rights is crucial in these situations.

The Long-Term Financial Damage

A judgment lien in Texas isn't some short-term headache. It stays active for a staggering ten years from the date it's recorded. And it gets worse. Creditors can often renew the judgment right before it expires, potentially locking up your property for another decade. This creates a long-lasting financial weight that can follow you for years, or even decades.

And the debt itself doesn’t just sit there.

Interest keeps piling up on the original judgment amount the entire time the lien is active. This means a debt that started at a few thousand dollars can balloon into a much larger sum over ten or twenty years, making it far harder to ever pay off.

This compounding interest is the hidden danger many property owners miss. Ignoring a lien doesn't make it disappear; it just makes it more expensive.

Understanding Non-Exempt Property and Your Homestead Rights

It's critical to know that a judgment lien in Texas can only attach to your non-exempt property. Texas law offers powerful protections for certain assets to keep creditors from taking everything you own. The single most important of these is the homestead exemption.

Under Chapter 41 of the Texas Property Code, your primary residence is generally considered your homestead and is protected from being seized by most creditors. In other words, a creditor usually can’t force you to sell your main home to pay off a judgment debt.

But this protection isn't a silver bullet. The rules have limits:

- The lien is still there: Even though your homestead is safe from a forced sale, the lien remains stuck to the property's title. You still can't sell or refinance your home until the debt is handled.

- It hits your other properties: If you own any other real estate—a vacation cabin, a rental property, or even a plot of raw land—those assets are considered non-exempt. They are completely vulnerable to the lien.

Navigating these laws can feel overwhelming. Understanding the line between exempt and non-exempt property is the key to protecting your assets and figuring out a plan to clear your title. An experienced attorney can help you assert your homestead rights and explore the best options for resolving the lien for good.

How a Creditor Gets a Judgment Lien on Your Property

To fight a lien, you first have to understand how it got there. A judgment lien doesn’t just materialize out of thin air. It’s the final prize a creditor gets after following a very specific legal playbook, and they have to follow it perfectly. Knowing their game plan helps you spot where they might have slipped up—and where you might have an opening to challenge the lien.

The whole thing starts long before any paperwork ever touches your property records. It begins in a courtroom.

A creditor, whether it’s a former landlord, a credit card company, or someone else you owe, must first take you to court and win a monetary judgment. This court order is the legal bedrock for everything that comes next.

Without that initial win in court, a creditor has no right to go after your property. This is why it is absolutely critical to respond to any lawsuit you receive. Ignoring a court summons is one of the most common and costly mistakes people make. It almost always results in a "default judgment," where the court sides with the creditor simply because you never showed up to tell your side of the story.

From a Courtroom Win to a Claim on Your Property

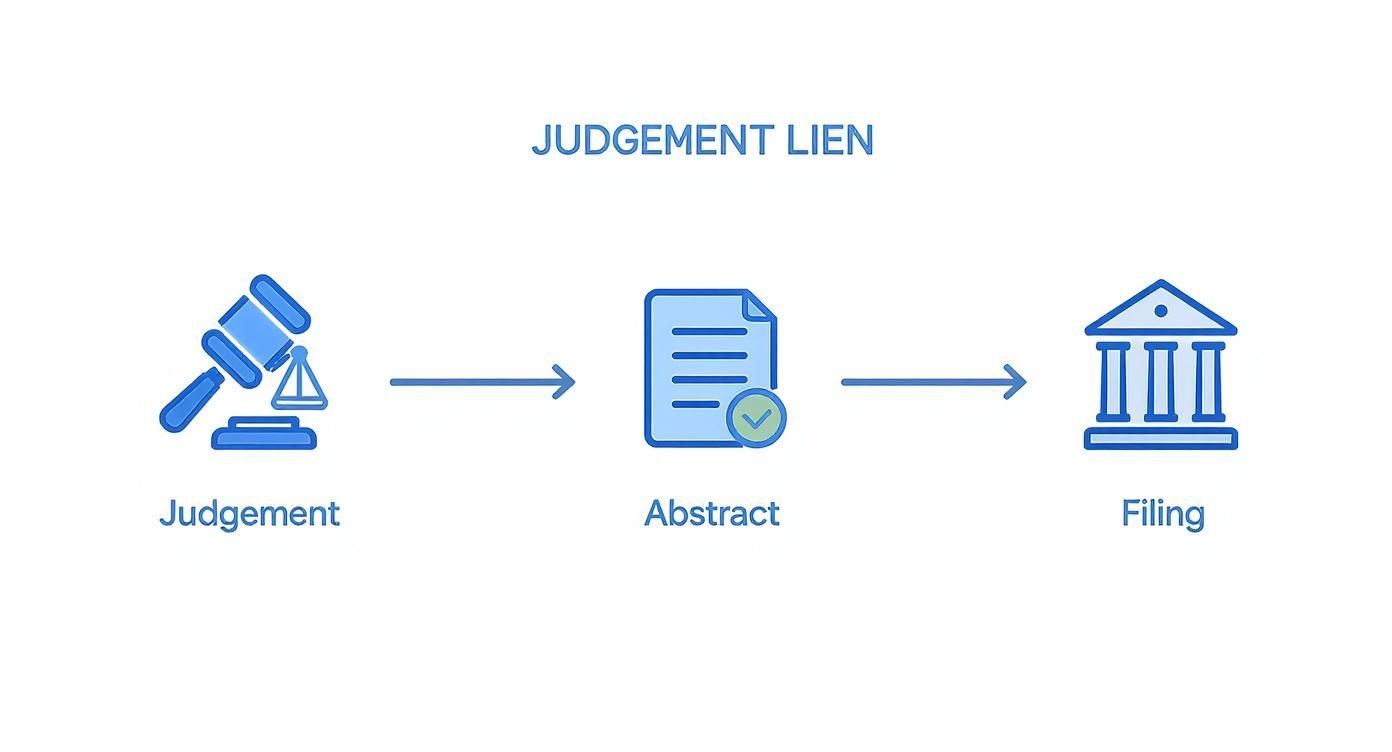

Once the creditor has that judgment in hand, they can finally make their move to secure the debt against your real estate. This is where they turn the court’s decision into a public, enforceable claim that can tie up your property for years.

This is where the Texas abstract of judgment comes in. The creditor goes back to the court clerk and asks for this special document. It's basically a one-page summary of the lawsuit: who owes the money, who gets paid, the judgment amount, and other key details.

This quick visual breaks down the simple, yet powerful, three-step process a creditor uses to turn a court victory into a lien on your real estate.

As the infographic shows, it's a procedural march—from a judge's ruling to a formal document and, finally, to a public record that directly clouds your property title.

The Final Step: Filing the Abstract

Here's the key: the abstract of judgment itself isn't the lien. The last and most important step is for the creditor to take that document and file it with the county clerk's office. The lien officially latches onto your property the second it’s recorded in the county’s real property records.

A smart creditor won't just file it in one county, either. It’s a common strategy to file the abstract in every single Texas county where you might own property now or in the future. This gives them maximum leverage, as the lien will automatically attach to any non-exempt real estate you own—or buy—in those counties for the next 10 years.

And Texas courts are busy. For example, during Fiscal Year 2024, the Second Court of Appeals in Texas handled 1,069 new cases, and more than half of those were civil matters that could end in these types of judgments.

Under Texas Property Code § 52.001, the proper recording of the abstract of judgment is what actually creates the lien. If the creditor botches the filing with the county clerk, no legal lien is created, no matter what the judge ordered.

This entire process shows how a private lawsuit can escalate into a very public claim against your most valuable assets. It also drives home why acting fast is your best defense. What seems like a minor legal issue can snowball quickly, and understanding these steps is the first move you can make to protect your property. This path from court order to real-world consequence is common in Texas law, and learning more about the eviction process in Texas can offer more insight into how these legal mechanisms work.

How to Remove a Judgment Lien in Texas

Finding a lien slapped on your property is a gut-punch, but it’s not the end of the road. You have clear, actionable ways to get that judgment lien removed and take back full control of your real estate. This is where you stop playing defense and start taking strategic steps to clear your title for good.

Here is a step-by-step guide to resolving the issue:

Step 1: Pay the Debt in Full to Get a Release of Lien

The most direct path, without a doubt, is to just pay the debt in full. That means the original judgment amount plus any post-judgment interest that has stacked up over the years. Once the creditor has the full payment in hand, they are legally required to sign a document called a "Release of Lien."

This release is the official "all clear" signal, stating the debt is satisfied. You or the creditor then need to file this document with the very same county clerk where the original abstract of judgment was recorded. Filing the release scrubs the lien from your property records, finally lifting the cloud from your title.

It's straightforward, but let's be honest—it's not always possible, especially if the debt has ballooned over time. Still, it provides a clean, final end to the problem.

Step 2: Negotiate a Settlement with the Creditor

If paying the whole thing isn't in the cards, your next best move is often negotiation. Think about it from the creditor's perspective: many would rather get a guaranteed chunk of cash now than wait around for years, hoping to maybe, someday, collect the full amount. This gives you some real leverage to negotiate a settlement—an agreement where you pay a smaller, lump-sum amount to wipe out the entire debt.

Real-World Scenario: A creditor holding a $10,000 judgment might jump at the chance to accept $5,000 today just to close their books and be done with it. When you're negotiating, keep these steps in mind:

- Start with a real offer: Propose a lump-sum payment you can actually make.

- Get it all in writing: Never, ever send money without a signed settlement agreement that clearly says your payment satisfies the debt in full.

- Make the Release of Lien part of the deal: The written agreement must state that the creditor will provide a signed Release of Lien as soon as they get your payment.

This takes some communication and a little bit of back-and-forth, but it can save you a serious amount of money and get the lien off your property.

Step 3: Challenge the Validity of the Lien

Sometimes, the lien itself is fundamentally flawed. A Texas abstract of judgment has to follow a very strict set of rules, and a single mistake can make the whole thing invalid. You might be able to challenge the lien in court if you uncover problems like:

- Improper Filing: The abstract was recorded incorrectly or is missing key information required by the Texas Property Code.

- Expired Judgment: The judgment is more than ten years old and the creditor never bothered to properly renew it. At that point, it becomes dormant and can't be enforced without a whole new court process.

- Exempt Property: The lien was attached to your homestead, which is protected from most creditors under Texas law.

Here’s a classic scenario: a homeowner tries to refinance their house, only to discover a decade-old judgment lien they'd forgotten about. Their attorney digs into the county records and finds the abstract was never renewed before it went dormant. This gives them immense leverage to negotiate a massive discount for its removal, since the creditor now faces a tough, uphill legal battle to revive it.

Challenging a lien is a more complex legal game, and it’s one where you'll almost certainly need an experienced Texas attorney in your corner. If you win, though, the court can order the lien to be removed entirely—without you having to pay a dime of the original debt. An attorney can dissect the abstract, pinpoint its weaknesses, and give you a clear strategy to get your property title clean again.

Why These Old Records Still Pack a Punch Today

The Texas abstract of judgment isn't some new-fangled legal trick. It's a powerful tool with roots that run deep into the state’s history, shaping property law for more than a century. Grasping this history helps you understand why these public records carry so much weight with lenders, title companies, and courts today.

When you're dealing with a judgment lien, you're not just up against a recent problem. You're interacting with a system built on decades of legal principles designed to protect property rights and give everyone fair notice of outstanding debts.

A Legacy Locked in County Archives

This whole practice of publicly recording judgments has been a cornerstone of Texas law for generations. This isn't an exaggeration—historical archives show this system has been running nonstop for over 100 years.

Take a look at the archives in Travis County, for example. You’ll find dusty old books detailing abstracts of judgment filed and recorded between 1905 and 1919. These century-old documents prove just how seriously the state has always taken these vital public records. You can even explore these historical abstracts to see this long-standing legal tradition for yourself.

This unbroken line of history is exactly why a Texas abstract of judgment is so formidable. It's not just a piece of paper; it's part of a time-tested process that the entire real estate world relies on for stability.

An abstract of judgment isn't a temporary issue. It's a formal, public claim built on a legal framework that's stood for over a hundred years—which is why you need a rock-solid legal strategy to deal with it.

How the Past Shapes Your Present Fight

So, why does any of this old history matter to you right now?

Because it proves the system is stable, predictable, and designed to be taken seriously. When a title company pulls your property records, they're plugging into a historical database that serves as the very bedrock of property ownership in Texas.

This perspective makes one thing crystal clear: resolving a lien isn't just about paying off a debt. It's about clearing your name from a permanent public record. Because these documents have such a long and significant history, they can't be wished away or ignored.

The only way to truly close this chapter is by securing a formal Release of Lien and making damn sure it's recorded correctly. An experienced Texas landlord-tenant lawyer can walk you through this critical process and help you navigate this time-honored system.

Your Questions Answered: Judgment Liens in Texas

When you're dealing with property law, things can get confusing fast. And when a judgment lien is involved, you need clear, straightforward answers. Here are some of the most common questions we hear from Texas property owners, explained in plain English.

Can a Creditor Put a Lien on My Primary Home?

This is usually the first and most urgent question on everyone's mind. The short answer in Texas is generally no—a creditor can't force the sale of your primary residence to satisfy a judgment debt.

Why? Because of the powerful homestead protections built into the Texas Constitution and detailed in Chapter 41 of the Texas Property Code. Your homestead is considered exempt property. But—and this is a big but—the lien still attaches to your property's title. It creates a "cloud" that effectively stops you from selling or refinancing until the debt is paid.

How Long Does a Judgment Lien Last in Texas?

Once a judgment lien is recorded in the county records, it stays active and enforceable for ten years.

It's critical to understand that this isn't a "set it and forget it" situation. Creditors can, and often do, renew the judgment before that ten-year clock runs out, which starts another ten-year countdown. You can't just wait for it to go away on its own; clearing your title almost always requires taking direct action.

What Happens if I Just Ignore the Lien?

Ignoring a judgment lien is one of the biggest mistakes you can make. While your homestead might be safe from a forced sale for now, the problem doesn't disappear—it gets worse.

The debt doesn't just sit there—it grows. Interest keeps piling up on the judgment amount for as long as the lien is active. Over a decade, that can make the total you owe skyrocket.

On top of that, the lien will continue to cloud your title, making it impossible to sell your property or get a new loan. Sooner or later, you or your heirs will have to confront a much larger, more complicated debt to get a clear title.

How Can I Find Out if My Property Has a Lien?

Thankfully, checking for a lien is a pretty straightforward process. You have two main options to see what's going on with your property's title:

- Search County Records: Head down to the county clerk’s office where your property is located and look through the real property records under your name. Many counties now have these databases online, which makes the search even easier.

- Hire a Title Company: For a more comprehensive search, a local title company is your best bet. They are experts in digging through property records and can give you a full report on any liens, judgments, or other issues attached to your title.

Knowing where you stand is the first step to taking back control.

If you need help with a judgment lien, lease issue, or rental dispute, contact The Law Office of Bryan Fagan, PLLC for a free consultation today.

![Graphic design featuring the title "8 Valid Reasons to Break a Lease in Texas [2025 Guide]" with decorative elements like a pen and paper, emphasizing tenant rights and legal guidance in Texas.](https://texastenantlawyers.com/wp-content/uploads/2025/11/featured-image-7ebe2aec-eacb-4e61-8e85-9c298b07ad11.jpg)